The Modality Death Clock: What Cycling’s Collapse From Dominant to 4% of New Openings Tells You About Infrared’s Franchise Lifespan

Indoor cycling didn’t decline gradually. It collapsed within a single franchise agreement term — and the investors who signed 10-year deals at the peak are still locked in.

Introduction

You’re evaluating a Hotworx franchise. Ten-year agreement. $300K+ total investment. The fundamental bet: that infrared fitness will still attract paying members throughout your entire contract term.

Before you make that bet, look at what happened to the last three “revolutionary” boutique fitness formats — and consider what the infrared trend science analysis reveals about durability:

- Indoor cycling went from the dominant boutique modality to 4% of new studio openings in 2026. Participation dropped 33.5% over six years.

- Barre fell from a top-three format to 2% of new openings. ClassPass data shows barre bookings down over 40% from their 2018 peak.

- Pilates surged from niche to 46% of all new boutique studio openings and 39.6% participation growth over the same six-year window.

These aren’t gradual evolutions. They’re modality collapses that happen within 4–6 years — well within a single franchise term.

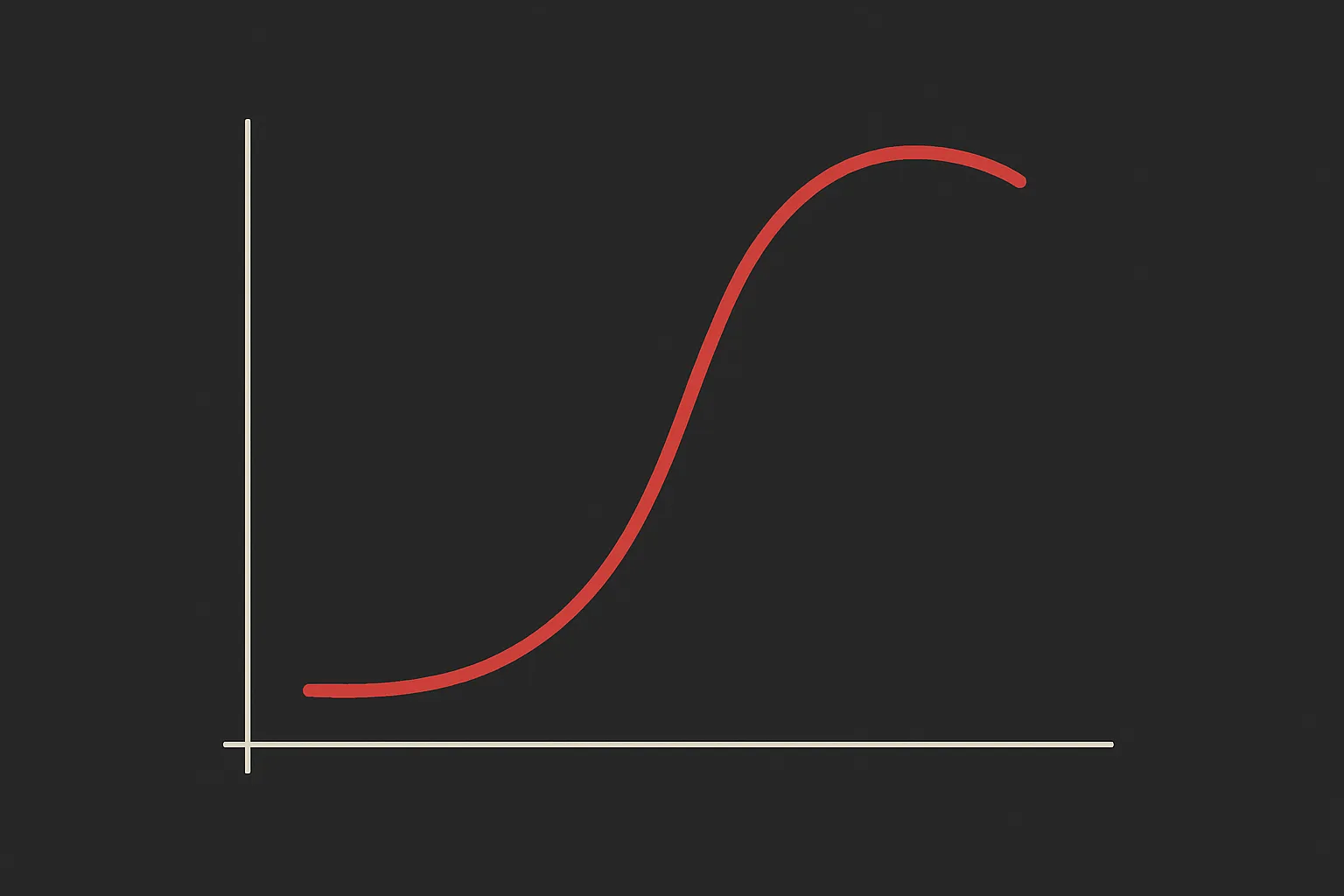

How Modality Collapse Actually Works

The franchise industry treats modality risk as binary: either it’s a fad or it’s not. But the data reveals a more specific pattern:

Phase 1: Novelty Premium (Years 1–3)

The format is new. Media coverage drives awareness. Early adopters pay premium prices for perceived exclusivity. Studios open rapidly.

Phase 2: Saturation Signal (Years 3–5)

Studio count peaks. Competition within the modality compresses margins. The consumer base who will ever try this format has largely tried it. Growth comes from market share, not market expansion.

Phase 3: Modality Substitution (Years 5–8)

A newer format absorbs the consumer’s attention and discretionary fitness spend. The transition happens faster than operators expect because boutique fitness members are inherently novelty-seeking — they chose a specialized studio over a general gym precisely because of the differentiated experience.

Phase 4: Structural Decline (Years 8+)

Not extinction — cycling studios still exist. But the addressable market contracts permanently. New openings drop to single digits. Existing operators compete for a shrinking member pool. Resale values collapse.

SoulCycle’s trajectory is the cautionary tale: from $900M+ valuation in 2015 to financial distress and mass studio closures by 2023, compressed into an 8-year window.

Where Infrared Sits on the Clock

Hotworx launched in 2017. It’s now year 9 of the concept’s commercial life. By the modality lifecycle pattern, this places infrared fitness somewhere in Phase 2–3 — past the novelty premium but before definitive substitution.

Arguments That Infrared Avoids the Pattern

- It’s not a single exercise format. Hotworx offers yoga, Pilates, cycling, HIIT, and isometrics — all inside infrared saunas. If the underlying modality shifts (cycling → Pilates), Hotworx can theoretically shift programming without changing infrastructure.

- The heat element is the differentiator, not the exercise. Cycling competed against other cycling studios. Hotworx competes as “infrared” — the sauna is the value proposition, not the specific workout inside it.

- Recovery/wellness positioning provides a second demand driver. Even if “infrared fitness” cools, “infrared wellness/recovery” may sustain interest as the broader wellness market grows to $6.3 trillion globally.

Arguments That Infrared Is Following the Pattern

- Nine years is late-cycle by historical standards. Cycling’s dominance lasted roughly 2012–2019 (7 years from mainstream adoption to decline). Barre peaked around 2015–2019 (4 years). Infrared at year 9 is already older than most modality cycles.

- Competitor proliferation mirrors Phase 2. Perspire Sauna Studio reaching 100 locations, Red Effect expanding, Glow Sauna emerging, plus infrared additions at general wellness studios — the saturation signal is present.

- The “it’s different because wellness” argument was made about barre too. Barre positioned as mind-body, injury-prevention, flexibility — not just fitness. It still collapsed to 2% of openings.

- Hotworx’s 800+ studio count means the early-adoption premium is gone. At 800+ U.S. studios, infrared isn’t novel. The consumer who was going to try infrared based on curiosity has largely done so.

The Franchise Agreement Trap

Here’s what makes modality risk uniquely dangerous in a franchise context versus an independent studio:

You can’t pivot. An independent infrared studio owner watching cycling collapse could rebrand as a Pilates/infrared hybrid, add contrast therapy, or completely change the concept. A Hotworx franchisee is contractually bound to the Hotworx format for 10 years. The franchise agreement controls programming, equipment, branding, and service offerings.

Your transfer value is modality-dependent. If infrared sentiment shifts during your term, your studio’s resale value doesn’t just decline proportionally — it collapses. Buyers applying franchise valuations to a declining-modality concept apply deep discounts. Hotworx’s transfer requirements add friction that further compresses exit values when the market turns.

The franchisor’s incentive isn’t aligned. Hotworx Corporate earns the flat $399/month royalty whether your studio is thriving or struggling. If modality sentiment shifts, their rational response is continued franchise sales (new unit fees) into markets where existing units are declining — exactly what happened with SoulCycle and Flywheel in cycling’s late Phase 2.

What This Means for Your Investment Decision

This piece isn’t arguing that infrared WILL collapse on a specific timeline. It’s arguing that modality lifecycle risk is real, documented, and fast-moving — and your investment model should account for it explicitly.

The Modeling Exercise

Run three scenarios:

- Base case: Infrared follows the wellness-supported trajectory. Demand stabilizes (doesn’t grow) at current levels through your franchise term. Model flat revenue, no real growth.

- Downside case: Infrared follows the cycling pattern with a 3–5 year lag. Revenue peaks in years 1–3, then declines 15–25% through years 4–10 as a newer modality absorbs consumer attention. Model declining revenue and a compressed exit multiple.

- Optimistic case: The “it’s wellness, not just fitness” thesis holds. Infrared maintains or grows demand through the term. Model 5–8% annual revenue growth.

The franchise agreement locks you in for all three scenarios. Your break-even analysis should survive the downside case — not just the base case — because the cycling precedent demonstrates that modality collapse IS the realistic downside, not a theoretical worst-case.

Three Signals to Watch

Before signing, track these leading indicators of where infrared sits on the lifecycle:

- New studio opening velocity vs. closure rate. Hotworx’s Item 20 disclosure shows closures. If net new openings decelerate while closures accelerate, you’re entering Phase 3.

- Member acquisition cost trends. Ask franchisees in validation: is it getting harder or easier to sign new members compared to 12–18 months ago? Rising CAC is the earliest financial signal of saturation.

- Competitor density in your target DMA. Count every infrared-offering facility (not just Hotworx) within a 15-minute drive of your proposed location. If the number doubled in the last 24 months, the saturation clock is ticking.

The Bottom Line

Every franchise modality has a lifespan. Cycling’s was ~7 years from mainstream to decline. Barre’s was ~4 years. The historical range for boutique fitness modality relevance is 5–10 years from mainstream adoption to structural demand decline.

Infrared fitness hit mainstream in 2017–2018. It’s now year 8–9. Whether the clock gives you 2 more years or 6 more years is unknowable — but the clock exists, and pretending it doesn’t is a modeling failure.

Your franchise agreement commits you to a 10-year term. Make sure your financial model works even if the modality’s best years are already behind it.

The question isn’t whether infrared is legitimate today — it clearly is, with 800+ studios and 400,000+ claimed members. The question is whether it will be equally compelling to consumers in year 7 of your agreement. History suggests you should model both answers.

This analysis is editorially independent and not affiliated with, endorsed by, or sponsored by Hotworx or any franchise system.