The Reinvention Tell: What FX Zone, Thunder Row, Pro Shop Overhaul, and “Revolution” Messaging Reveal About Infrared’s Revenue Ceiling

When a franchise built on infrared saunas starts adding battle ropes, rowing machines, and a retail payment overhaul — all at once — the question isn’t innovation. It’s whether the original concept could stand alone.

Four Signals, One Message

When a franchise built entirely on infrared saunas starts adding battle ropes, rowing machines, and a retail payment overhaul — all at once — the question isn’t whether the brand is innovating. It’s whether the original concept ever generated enough revenue to stand on its own.

Hotworx launched in 2017 with a clean, differentiated premise: infrared sauna workouts in private pods. No barbells. No mirrors. No conventional gym clutter. The pitch to franchisees was simplicity — small footprint, low labor, technology-driven fitness.

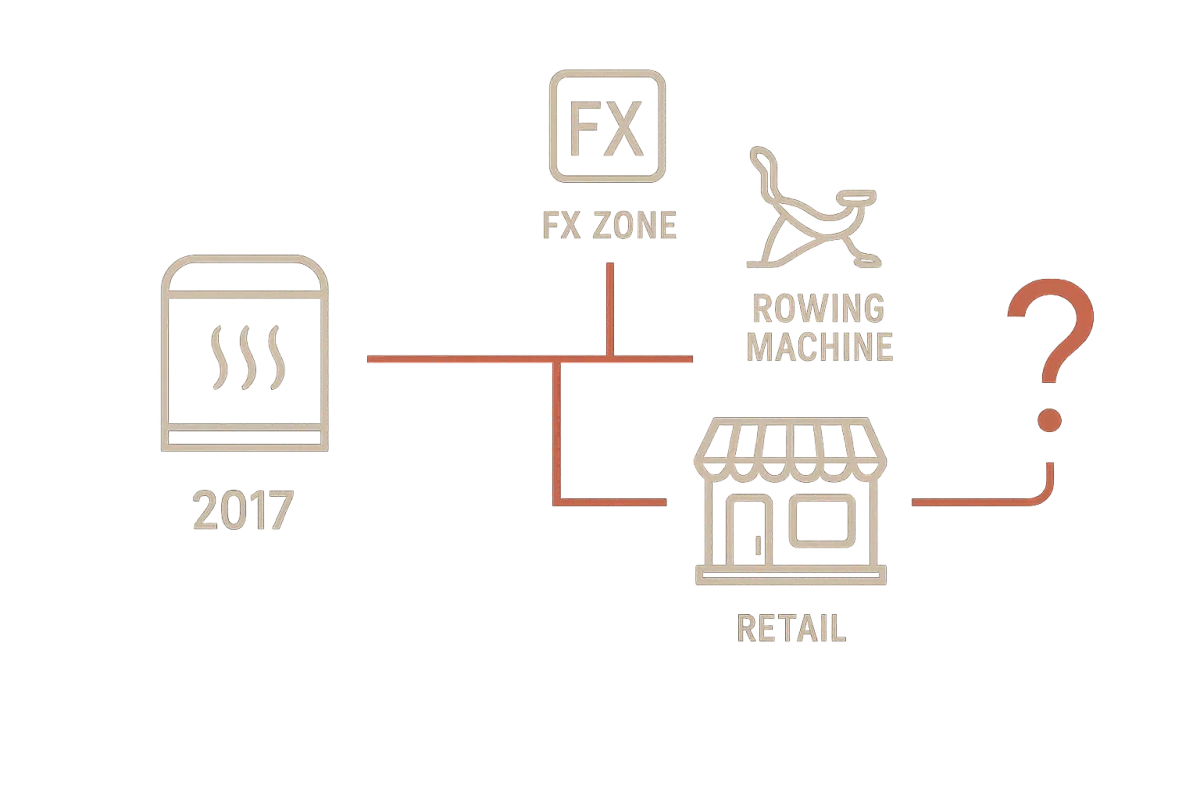

Nine years and roughly 800 studios later, the franchisor is simultaneously rolling out four major additions: Project Sledge Hammer (the FX Zone functional training area), Thunder Row (a proprietary rowing machine), a complete pro shop payment system overhaul, and a branding campaign called “Reinvention to Revolution” positioning all of it as visionary evolution. If you’re deep in due diligence, you need to read these moves together — not as four innovations, but as one signal.

That signal is concept diversification. And concept diversification, in franchise analysis, is the clearest indicator that a system’s core revenue engine is underperforming.

The Pattern Nobody’s Naming: Four Simultaneous Additions Aren’t Expansion — They’re a Pivot

Healthy franchise systems iterate. They optimize unit economics within their existing model. They improve operations manuals, tighten supply chains, refine marketing playbooks. What they don’t do is launch four net-new revenue categories in a single cycle while median unit volumes are declining.

Consider what Hotworx is adding simultaneously:

- FX Zone / Project Sledge Hammer: A dedicated functional training area with conventional equipment — battle ropes, kettlebells, TRX suspension bands, slam balls, plyo boxes. This is standard gym equipment that exists in every CrossFit box and boutique fitness studio in the country.

- Thunder Row: A proprietary rowing machine featuring a 360-degree handle swivel and dual water turbo tanks. Proprietary means single-source supply chain, franchisor-controlled pricing, and no aftermarket parts.

- Pro shop payment overhaul: A rebuilt retail transaction system, signaling that the existing retail revenue stream was either underperforming or operationally broken.

- “Reinvention to Revolution” messaging: A deliberate rebrand of the entire initiative as forward-looking strategy rather than corrective action.

Any one of these in isolation looks like smart product development. All four at once, announced while system-wide AUV sits at $291K against an industry median of $556K and year-over-year unit volumes have dropped 11.2% according to FranchisePayback.com, looks like a franchisor scrambling to find revenue that infrared alone isn’t delivering.

The distinction matters because it changes what you’re buying. You’re not buying a proven concept with incremental enhancements. You’re buying a concept in active transformation — and the financial performance data in the FDD reflects the old version, not the new one.

What the FX Zone Really Tells You: Infrared Alone Wasn’t Enough

The FX Zone is the most revealing addition because it directly contradicts the founding thesis. Hotworx’s entire market positioning was built on not being a conventional gym. No free weights. No functional training floors. No equipment that requires supervision, cleaning protocols, or injury liability beyond the controlled sauna environment.

Adding battle ropes, kettlebells, and TRX bands means one of two things. Either members were churning because the infrared-only offering couldn’t sustain long-term engagement, or the franchisor concluded that new member acquisition requires a broader pitch than “infrared sauna workouts.”

Both explanations point to the same underlying problem: the core concept has a revenue ceiling.

This isn’t speculation. The numbers support it. The 2026 FDD’s Item 19 financial performance representation shows median AUV of $291K — a figure we break down in detail in the 2026 FDD Item 19 breakdown. That $291K is roughly 52% of the fitness franchise industry median tracked by Frandera. The system isn’t just underperforming relative to competitors. It’s underperforming relative to its own trajectory, with the -11.2% year-over-year decline suggesting deceleration, not maturation.

The FX Zone is the franchisor’s implicit admission that the sauna pods alone don’t generate enough visits per member per month to sustain healthy unit economics. Functional training equipment is designed to give members a reason to come more often, stay longer, and perceive more value — all things the infrared concept apparently wasn’t accomplishing at sufficient scale.

For prospective investors, the question is direct: if you’re underwriting a Hotworx franchise based on the simplicity of the infrared model — low labor, small footprint, minimal equipment maintenance — does the FX Zone invalidate that thesis? Battle ropes break. Kettlebells need racks. Slam balls need replacement. TRX bands need inspection. You’ve just added the operational complexity the concept was designed to avoid. Review the equipment lifecycle and year-5 capex analysis to understand what that complexity costs over a franchise term.

Thunder Row and the Proprietary Equipment Trap: Capital You Didn’t Budget For

Thunder Row deserves its own scrutiny because proprietary equipment changes the franchise relationship in ways that don’t show up in the initial investment table.

The rowing machine features a 360-degree handle swivel and dual water turbo tanks. These are custom-engineered, Hotworx-specific components. That means:

- Single-source dependency. You buy it from the franchisor or an approved supplier. There is no competitive bidding. There is no aftermarket alternative.

- Franchisor-controlled pricing. The markup between manufacturing cost and franchisee purchase price is opaque. Franchise systems routinely generate 20–40% gross margins on proprietary equipment sales to franchisees.

- Maintenance and replacement on the franchisor’s terms. When a dual water turbo tank fails — and mechanical components fail — you’re buying the replacement part from one source at one price.

- No residual value. If you exit the franchise, proprietary equipment has no secondary market. It’s worthless outside the system.

This is the proprietary equipment trap that experienced franchise investors recognize immediately. The franchisor creates a product that only exists within its ecosystem, sells it to franchisees at a markup, controls the replacement cycle, and captures margin on every transaction. It’s a profit center for the franchisor that appears as a cost center on the franchisee’s P&L.

The critical due diligence question: is Thunder Row included in the current initial investment range in Item 7, or will it be a post-opening capital requirement? If you’re signing an agreement today based on a $300K–$600K buildout estimate, and Thunder Row units cost $3,000–$8,000 each (typical range for commercial rowing machines, and proprietary versions run higher), you need 6–10 units per studio to create a meaningful “Thunder Row” section. That’s $18K–$80K in unbudgeted capital expenditure.

This stacks on top of existing equipment replacement cycles that are already more expensive than most prospective franchisees model. We detail those costs in the hidden monthly operating costs breakdown.

The Pro Shop Overhaul: Fixing Revenue or Creating the Illusion of It?

A payment system overhaul for the pro shop tells you the existing retail operation was broken. Functional payment systems don’t get rebuilt. They get updated. An overhaul means the franchisor identified material revenue leakage, transaction friction, or reporting gaps that were suppressing retail performance.

The optimistic read is that the old system was leaving money on the table and the new system will capture it. The realistic read is that retail revenue in a fitness franchise is a margin supplement, not a margin driver.

Industry benchmarks for boutique fitness retail (apparel, supplements, accessories) typically run 3–8% of total revenue. At $291K AUV, that’s $8,700 to $23,300 annually. Even if the new payment system doubles retail capture rates, you’re talking about $8,700 to $23,300 in incremental revenue — meaningful on a percentage basis, but not transformative on a dollar basis.

The risk is that the franchisor uses improved retail reporting to inflate perceived unit performance without changing the underlying membership economics. A studio that generates $291K from memberships and $15K from retail is a $306K unit. That’s still 45% below the industry median. The pro shop didn’t close the gap. It papered over it.

Watch for how the franchisor presents retail revenue in future FDD updates. If pro shop income gets blended into top-line AUV without breakout reporting, you’re losing visibility into the metric that actually matters: membership revenue per square foot.

The Financial Mismatch: Which Concept Does the FDD’s $291K Reflect?

This is the most consequential question for anyone modeling a Hotworx investment right now.

The $291K median AUV in the 2026 FDD reflects studios operating under the original concept — infrared sauna workouts, existing equipment packages, existing pro shop configuration. It does not reflect studios with the FX Zone installed. It does not reflect Thunder Row revenue contribution. It does not reflect the upgraded pro shop payment system.

You are looking at historical financial performance for a concept the franchisor is actively replacing. As explored in the unit economics owner profit model, that $291K figure already produces thin margins after rent, royalties, marketing fund contributions, labor, and equipment maintenance. The franchisor is betting that concept diversification will push that number higher. But you’re signing an agreement and writing a check based on the number that exists today.

First-year studio revenue data tracked by 1851 Franchise suggests ramp periods of 12–18 months for boutique fitness concepts. If you open a studio with the new configuration, your first 18 months of revenue will have no historical comp in the FDD. You’re a beta tester for an unproven format, paying full franchise fees for the privilege.

Investors working with firms like Lendesca to model franchise financing scenarios should note that concept evolution of this magnitude changes the underwriting thesis entirely — you’re financing a different business than the one the performance data describes.

The FDD’s financial performance representations are backward-looking by design. They tell you what happened. They cannot tell you what will happen when the concept changes. This gap between reported performance and projected performance is where franchisee capital is most at risk.

The “Revolution” Framework: How to Read Franchisor Messaging Like a Due Diligence Pro

The Franchising.com article from June 2026 positions all of this under a “Reinvention to Revolution” narrative. The language is important. “Reinvention” acknowledges that the existing model needed changing. “Revolution” frames that change as visionary rather than corrective.

Experienced franchise analysts read this messaging through a simple filter: what problem is the franchisor solving, and who identified it?

If franchisees demanded more equipment variety because members were churning, the problem is retention — and the solution is defensive. If the franchisor identified a market opportunity to expand the concept’s addressable market, the problem is growth — and the solution is offensive. The messaging doesn’t distinguish between these, and that ambiguity is deliberate.

Here’s what to look for in your own diligence:

- Validation council feedback. Ask the franchisor for franchisee advisory council minutes or feedback summaries related to the FX Zone and Thunder Row decisions. If franchisees requested these additions, it confirms a retention or engagement gap.

- Pilot studio performance data. Have any studios already installed the FX Zone or Thunder Row? What did their revenue look like before and after? If no pilot data exists, the system is rolling out unvalidated changes to 800+ locations.

- Item 7 amendments. Check whether the franchisor has filed or is planning to file an amended FDD with updated initial investment ranges reflecting the new equipment requirements.

- Franchisee capex obligations. Are existing franchisees required to install these additions? On what timeline? At what cost? Who absorbs the buildout — the franchisee, the franchisor, or a cost-share arrangement?

- Competitive positioning shift. With the FX Zone, Hotworx now competes directly with F45 Training, Orangetheory, and other functional fitness concepts. Review whether the franchise agreement’s territory protections account for this expanded competitive set.

The broader pattern is documented in franchise operations research. As Franchise Times has reported, fitness franchise systems that maintain operational discipline around a focused concept tend to outperform systems that diversify in response to unit-level performance pressure. Diversification spreads management attention, increases operational complexity, and raises capex requirements — all headwinds for a franchisee operating a single unit.

What This Means for Your Investment Decision

None of this means Hotworx is a bad investment. It means the investment thesis has changed, and your diligence needs to change with it.

You are no longer evaluating “infrared sauna workouts in a simple, low-labor format.” You are evaluating a hybrid fitness concept that combines infrared technology with conventional functional training, proprietary cardio equipment, and an expanded retail operation. That’s a fundamentally different business with different capital requirements, different competitive dynamics, and different operational complexity.

The FDD’s financial performance data doesn’t reflect this new reality. The franchisor’s marketing materials promote the vision. The gap between those two things is where your risk lives.

Three actions before you proceed:

- Re-model your unit economics with FX Zone and Thunder Row capex included. Add $30K–$80K to your buildout estimate and model the incremental maintenance costs over a 10-year franchise term. Start with the equipment lifecycle and year-5 capex analysis.

- Talk to franchisees operating mature studios (3+ years) about member engagement and retention trends before any new equipment was announced. Their experience is the closest proxy for the concept you’d actually be operating during your ramp period.

- Assess the infrared differentiator independently. If the core technology is being diluted by conventional equipment additions, evaluate whether the infrared component still provides meaningful market differentiation — or whether it’s becoming a marketing feature rather than a business model. Our infrared trend risk assessment covers the science and market trajectory.

The franchisor calls it a revolution. The numbers call it a $291K AUV declining at 11.2% year-over-year. Your job as an investor is to figure out which narrative your capital is actually betting on.

This analysis is editorially independent and not affiliated with, endorsed by, or sponsored by Hotworx or any franchise system discussed.